Information related to the thematic semester on « Commodity Derivatives Markets » and the closing conference to be held in Paris on November 6th can be found on the following website:

Information related to the thematic semester on « Commodity Derivatives Markets » and the closing conference to be held in Paris on November 6th can be found on the following website:

Information related to the thematic semester on « Commodity Derivatives Markets » and the closing conference to be held in Paris on November 6th can be found on the following website:

by Ivar Ekeland and Maurice Queyranne

by Ivar Ekeland and Maurice Queyranne

In open pit mining, one must dig a pit, that is, excavate the upper layers of ground before reaching the ore. The walls of the pit must satisfy some mechanical constraints, in order not to collapse. The question then arises how to mine the ore optimally, that is, how to find the optimal pit. We set up the problem in a continuous (as opposed to discrete) framework, and we show, under weak assumptions, the existence of an optimum pit. For this, we formulate an optimal transportation problem, where the criterion is lower semi-continuous and is allowed to take the value +∞. We show that this transportation problem is a strong dual to the optimum pit problem, and also yields optimality (complementarity slackness) conditions.

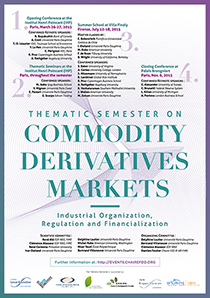

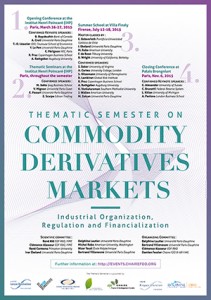

This project aims to examine recent developments in commodity derivatives markets. The changed industrial organization and the financialization of these markets are major phenomena, both of which call for changes in regulation.

Organized from March to November 2015, the thematic semester will include an opening conference, a series of thematic seminars, a summer school and a closing conference.

Link to the Thematic Semester’s webpage

by Anthony Lecavil, Nadia Oudjane & Francesco Russo

by Anthony Lecavil, Nadia Oudjane & Francesco Russo

We introduce a new class of nonlinear Stochastic Differential Equations in the sense of McKean, related to non conservative nonlinear Partial Differential equations (PDEs). We discuss existence and uniqueness pathwise and in law under various assumptions. We propose an original interacting particle system for which we discuss the propagation of chaos. To this system, we associate a random function which is proved to converge to a solution of a regularized version of PDE.

June 10-12 2015,

June 10-12 2015,

Paris (Institut Henri Poincare)

Further information on the Conference website

The conference is supported by:

The “Finance and Sustainable Development”Chair

The CEREMADE, Université Paris-Dauphine

The Laboratoire Jacques-Louis Lions

The Institut Louis Bachelier

The Projet ANR ISOTACE

The Institut Henri Poincaré

Université Franco-Italienne

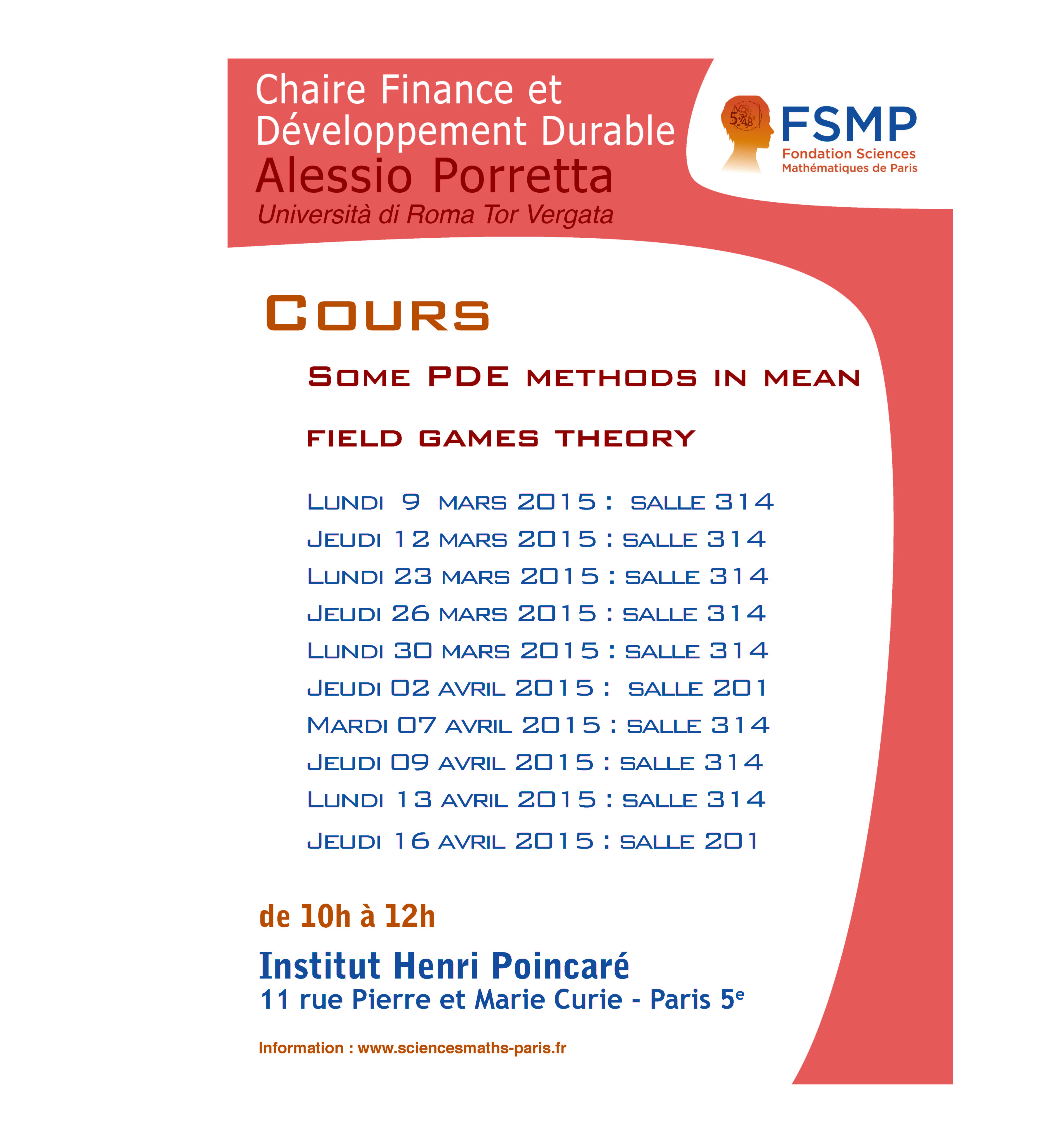

A Course by Professor Alessio Porretta

From March 9th to April 16th 2015

Institut Henri Poincaré (IHP), Paris

Mean field games theory was initiated by J.-M. Lasry and P.-L. Lions since 2006 in order to describe control processes with large number of agents (say, a population of identical individuals) whose strategy is influenced by the overall distribution of the agents. The macroscopic description, suggested as an asymptotic regime of Nash equilibria of N-players games when N goes to infinity, is given in terms of a new system of PDEs, where a backward Hamilton-Jacobi-Bellman equation (describing the individual strategy) is coupled with a forward Kolmogorov-Fokker-Planck equation (describing the evolution of the distribution law). The goal of this course is to present several problems and methods recently developed in the study of those systems, addressing questions such as the long time behavior and its connection with the turnpike property of controlled systems, the optimal transport of the distribution law, the well-posedness of weak theories and other possible related directions of research.

Further information on the FSMP Website

26-27 March 2015 – Institut Henri Poincaré (IHP), Paris

To launch the thematic semester, the opening conference will aim to show the state of the art and especially to identify new research problems. Special emphasis will be given to the identification of unsolved problems.

by Delphine Lautier, Franck Raynaud & Michel A. Robe

by Delphine Lautier, Franck Raynaud & Michel A. Robe

We apply the concepts of conditional entropy, information transfers and directed graphs to investigate empirically the propagation of price fluctuations across a futures term structure. We focus on price relationships for North American crude oil futures because this key market experienced several structural changes between 2000 and 2014: financialization (starting in 2003), infrastructure limitations (in 2008-2011) and regulatory changes (in 2012-2014) in addition to big demand and supply shocks in the underlying asset market. We find large variations over time in the amount of information shared by contracts with different maturities. Although on average short-dated contracts (up to 6 months) emit more information than backdated ones, a dynamic analysis reveals that, after 2012, similar amounts of information flow backward and forward along the futures maturity curve. The mutual information share increased substantially starting in 2004 but fell back sharply in 2012-2014. In the crude oil space, our findings point to a puzzling re-segmentation of the futures market by maturity in 2012-2014. More broadly, they have implications for the Samuelson effect and raise questions about the causes of market segmentation.

by Delphine Lautier, Julien Ling and Franck Raynaud

by Delphine Lautier, Julien Ling and Franck Raynaud

We examine the impact of two financial crises on commodity derivative markets: the subprime crisis and the bankruptcy of Lehman Brothers. These crises are “external” to the commodity markets because they occurred in the financial sphere. Still, because commodity markets are now highly integrated with each other and with other financial markets, such events could have had an impact. In order to fully comprehend this possible impact, we rely on tools inspired by the graph theory that allow for the study of large databases. We examine the daily price fluctuations recorded in 14 derivative markets from 2000 to 2009 in three dimensions: the observation time, the space dimension – the same underlying asset can be traded simultaneously in two different places – and the maturity of the transactions. We perform an event study in which we first focus on the efficiency of the price shock’s transmission to the commodity markets during the crises. Then we concentrate on whether the paths of shock transmission are modified. Finally, relying on the measure proposed by Bonacich (1987) for social networks, we focus on whether the centrality of the price system changes.

by René Aïd, Salvatore Federico, Huyên Pham & Bertrand Villeneuve

by René Aïd, Salvatore Federico, Huyên Pham & Bertrand Villeneuve

We establish explicit socially optimal rules for an irreversible investment decision with time-to-build and uncertainty. Assuming a price sensitive demand function with a random intercept, we provide comparative statics and economic interpretations for three models of demand (arithmetic Brownian, geometric Brownian, and the Cox-Ingersoll-Ross). Committed capacity, that is, the installed capacity plus the investment in the pipeline, must never drop below the best predictor of future demand, minus two biases. The discounting bias takes into account the fact that investment is paid upfront for future use; the precautionary bias multiplies a type of risk aversion index by the local volatility. Relying on the analytical forms, we discuss in detail the economic effects.

by Céline Grislain-Letrémy & Arthur Katossky

by Céline Grislain-Letrémy & Arthur Katossky

The willingness of households to pay for prevention against industrial risks can be revealed by real estate markets. By using very rich microdata, we study housing prices in the vicinity of hazardous industries near three important French cities. We show that the impact of hazardous plants on the housing values strongly differs among these three areas, even if the areas all surround chemical and petrochemical industries. We compare the results from both standard parametric and more flexible, semiparametric models of hedonic property. We show that the parametric model might structurally lead to important biases in the estimated value of the impact of hazardous plants on housing values and in the variations of this impact with respect to the distance from the plants.

by Antoine Rose

by Antoine Rose

Les initiatives de comptabilité des émissions de carbone se sont multipliées au cours des dernières années, à mesure que la problématique du changement climatique s’est imposée. Pour chaque agent économique, la problématique climatique se traduit par des questions, des enjeux et des objectifs différents, si bien qu’une diversité de comptabilités carbones s’est développée. Cet article propose d’examiner ces modèles comptables : Inventaires Nationaux, comptes NAMEA, Bilan Carbone) à travers leurs règles d’allocation des émissions de gaz à effet de serre (GES) aux acteurs et activités économiques. L’article replace ainsi les règles techniques des comptabilités carbones dans la perspective du débat plus fondamental autour de la définition de la responsabilité des agents économiques. Enfin il définit un nouveau type d’allocation des émissions de (GES) aux activités économiques, fondé sur le concept de « responsabilité fondamentale » : la « comptabilité carbone par enjeux ». Ce nouveau type de comptabilité est appliqué à la cartographie des émissions de GES induites par un portefeuille bancaire.

by Céline Grislain-Letrémy

by Céline Grislain-Letrémy

Insurance coverage for natural disasters remains low in many exposed areas. A limited supply of insurance is commonly identified as a primary causal factor in this low insurance coverage. The French overseas departments provide a rare natural experiment of a well-developed supply of natural disasters insurance in highly exposed regions. The French system of natural disasters insurance is underwritten and regulated by the French government; instituted initially for metropolitan France only, it was extended to overseas departments in the state of emergency following Hurricane Hugo in 1989. This natural experiment makes it possible to analyze the determinants of insurance coverage on the demand side. Based on unique household-level microdata, I estimate an insurance market model which had not yet been empirically tested. Using this structural approach, I show that underinsurance in the French overseas departments is neither due to perception biases nor to unaffordable insurance, but mainly to uninsurable housing and to the anticipation of assistance, which crowds out insurance. Individual insurance decisions are influenced by neighbors’ insurance choices through peer effects and neighborhood eligibility for assistance.

Publié dans Agathe Euzen, Laurence Eymard, Françoise Gaill (dirs). Le développement durable à découvert. CNRS Editions. 2013.

Publié dans Agathe Euzen, Laurence Eymard, Françoise Gaill (dirs). Le développement durable à découvert. CNRS Editions. 2013.

La question du développement est au cœur de la théorie économique. Malthus (1766-1834) a clairement identifié les deux limites, que la nature pose à la croissance de la population : la famine et la maladie. La révolution industrielle et scientifique a fait sauter ces deux barrières, et depuis, la population humaine et son niveau de vie sont engagés dans un processus de croissance exponentielle, de l’ordre de 3 % par an…

by Ivar Ekeland, Yiming Long & Qinglong Zhou

by Ivar Ekeland, Yiming Long & Qinglong Zhou

In economic theory, and in optimal control, it has been customary to discount future gains at a constant rate δ > 0 (…). That future gains should be discounted is well grounded in fact. On the one hand, humans prefer to enjoy goods sooner than later (and to suffer bads later than sooner), as every child-rearing parent knows. On the other hand, it is also a reflection of our own mortality: 10 years from now, I may simply no longer be around to enjoy whatever I have been promised. These are two good reasons why people are willing to pay a little bit extra to hasten the delivery date, or will require compensation for postponement, which is the essence of discounting. On the other hand, there is no reason why the discount rate should be constant, i.e. why the discount factor should be an exponential e−δt.

Conférence Les Nouveaux Outils du Développement Durable : Méthodes Quantitatives pour l’Economie et la Finance de l’Energie et des Ressources Naturelles

Université Paris Dauphine – Salle Raymond Aron – 24 & 25 octobre 2013

L’objectif de cette conférence est de faire le point sur les travaux réalisés depuis 7 ans au sein de la Chaire et au sein des « Initiatives de recherche », projets de recherche parrainés par la Chaire et ciblés sur des sujets plus précis (assurance récolte, microstructure des marchés financiers, finance des marchés de l’énergie…).

Autour de conférences invitées, six ateliers seront organisés sur 2 jours portant sur des méthodologies novatrices (jeux à champ moyen) ou des thèmes ciblés (les outils de la micro assurance pour les agriculteurs des pays en développement, la finance des marchés de l’énergie, etc). On alternera les présentations de chercheurs senior et les présentations de jeunes chercheurs.

par Sophie Laruelle

par Sophie Laruelle

Considérons qu’un trader ou un algorithme de trading interagissant avec les marchés durant les enchères continues puisse être modélisé par une procédure itérative ajustant le prix auquel il poste ses ordres à un rythme donné, (Laruelle, Lehalle & Pagès, 2013) propose une procédure minimisant son coût d’exécution. Ils prouvent la convergence p.s. de l’algorithme sous des hypothèses sur la fonction de coût et donnent des critères pratiques sur les paramètres du modèle qui assurent que les conditions pour utiliser l’algorithme sont vérifiées (notamment, en utilisant un principe de co-monotonie fonctionnel). Ici on va estimer les paramètres du flux d’exécution d’ordres. Tout d’abord on fait une étude de stabilité des paramètres et ensuite on construit des algorithmes adaptatifs pour estimer ces paramètres “en-ligne”.

by Aimé Lachapelle, Jean-Michel Lasry, Charles-Albert Lehalle & Pierre-Louis Lions

by Aimé Lachapelle, Jean-Michel Lasry, Charles-Albert Lehalle & Pierre-Louis Lions

This paper deals with a stochastic order-driven market model with waiting costs, for order books with heterogeneous traders. Offer and demand of liquidity drive price formation and traders anticipate future evolutions of the order book. The natural framework we use is mean field game theory, a class of stochastic differential games with a continuum of anonymous players. Several sources of heterogeneity are considered including the mean size of orders. Thus we are able to consider the coexistence of Institutional Investors and High Frequency Traders (HFT). We provide both analytical solutions and numerical experiments. Implications on classical quantities are explored: order book size, prices, and effective bid/ask spread. According to the model, in markets with Institutional Investors only we show the existence of inefficient liquidity imbalances in equilibrium, with two symmetrical situations corresponding to what we call liquidity calls for liquidity. During these situations the transaction price significantly moves away from the fair price. However this macro phenomenon is stabilized in markets with both Institutional Investors and HFT, although a more precise study shows that the benefits of the new situation go to HFT only, leaving Institutional Investors even with lower Profit & Loss.

by Gilles Chemla & Christopher A. Hennessy

by Gilles Chemla & Christopher A. Hennessy

What determines equilibrium securitization levels, and should they be regulated? To address these questions we develop a model where originators can exert unobservable effort to increase asset quality, subsequently having private information regarding quality when selling ABS to rational investors. In equilibrium, all originators have low/zero retentions if they are financially constrained and/or prices are sufficiently informative. Asymmetric information lowers effort incentives in all equilibria. Effort is promoted by junior retentions, investor sophistication, and informative prices. Optimal regulation promotes effort while accounting for investor-level externalities. It entails either a menu of junior retentions or a single junior retention with size decreasing in price informativeness. Mandated market opacity is only optimal amongst regulations failing to induce originator effort.

by Bertrand Villeneuve

by Bertrand Villeneuve

L’article modélise un programme de gestion de déchets nucléaires à haute activité. La physique du refroidissement permet d’entreposer un certain temps un colis chaud afin d’économiser le volume de stockage définitif : en effet, les colis plus froids peuvent être davantage serrés. La durée optimale théorique d’entreposage sans contrainte est caractérisée. Les diverses contraintes (contrainte sur la capacité de stockage, contrainte sur la durée d’entreposage, contrainte sur la capacité d’entreposage) sont envisagées. Elles conduisent à des traitements très différenciés selon les millésimes.